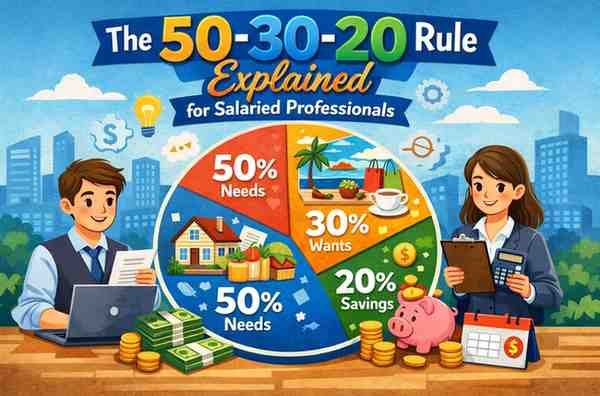

The 50-30-20 Rule Explained for Salaried Professionals

by financeretire · Published · Updated

Managing money effectively is a skill every salaried professional must master. No matter how much you earn, if your spending habits aren’t balanced, you may find yourself struggling by month-end. That’s where the 50-30-20 rule comes in — a simple yet powerful budgeting method that helps you spend, save, and invest smartly.

In this article, we’ll break down what the 50-30-20 rule is, how to apply it in real life, and why it’s perfect for salaried individuals in India.

1. What Is the 50-30-20 Rule?

The 50-30-20 rule is a personal finance formula designed to help you allocate your monthly income efficiently.

It divides your take-home salary into three clear categories:

-

50% for Needs

-

30% for Wants

-

20% for Savings and Investments

This method ensures you cover essentials, enjoy life, and still save for the future — without feeling restricted.

Formula:

👉 (Take-home Salary) = 50% Needs + 30% Wants + 20% Savings

2. Breakdown of the 50-30-20 Rule

Let’s understand each component with examples relevant to salaried professionals.

A. 50% — Needs (Essentials)

These are expenses you must pay every month to live comfortably. They are non-negotiable and form the foundation of your budget.

Examples of Needs:

-

House rent or home loan EMI

-

Groceries and household supplies

-

Electricity, water, and internet bills

-

Transportation or fuel

-

Health insurance premium

-

School fees or essential EMIs

💡 Tip: Try to keep your rent or home EMI under 25–30% of your income to maintain balance.

B. 30% — Wants (Lifestyle Expenses)

These are the things you enjoy but can live without. Wants make life enjoyable, but they should never exceed the limit — otherwise, they eat into your savings.

Examples of Wants:

-

Eating out and food delivery

-

Shopping, clothing, and gadgets

-

Vacations or weekend trips

-

OTT subscriptions (Netflix, Prime Video)

-

Gym memberships or entertainment activities

💡 Tip: You don’t have to cut out all fun — just plan it within the 30% budget.

C. 20% — Savings and Investments

This portion is for building your financial future. Saving and investing consistently will help you achieve long-term goals like buying a home, retiring early, or starting a business.

Examples of Savings and Investments:

-

Emergency fund contributions

-

SIPs in mutual funds

-

Equity or index fund investments

-

Recurring deposits or PPF

-

Retirement corpus (NPS or EPF)

-

Insurance premiums (life and health)

💡 Pro Tip: Automate your savings — set up a SIP or recurring transfer right after salary credit.

3. How to Apply the 50-30-20 Rule in Real Life

Let’s take an example.

Example:

If your monthly take-home salary is ₹80,000, your budget should look like this:

| Category | Percentage | Amount (₹) | Purpose |

|---|---|---|---|

| Needs | 50% | 40,000 | Rent, groceries, bills, fuel |

| Wants | 30% | 24,000 | Dining, shopping, entertainment |

| Savings & Investments | 20% | 16,000 | SIPs, insurance, emergency fund |

This gives you a balanced structure — you can enjoy your salary, cover essentials, and still grow your wealth.

4. Benefits of the 50-30-20 Rule

✅ Simple and Easy to Follow

You don’t need advanced financial knowledge — just basic awareness of your expenses.

✅ Builds Financial Discipline

It helps prevent overspending and ensures consistent savings every month.

✅ Balances Lifestyle and Savings

You enjoy life without guilt while planning for future goals.

✅ Adaptable for All Income Levels

Whether you earn ₹25,000 or ₹2 lakh, the percentage-based system works equally well.

✅ Encourages Early Investing

By allocating 20% toward savings, you automatically create long-term wealth.

5. Adapting the Rule to Your Salary

Everyone’s financial situation is different. You can tweak the ratio slightly depending on your goals.

Examples:

-

If you’re paying high rent (like metro cities): Use 60-20-20.

-

If you’re saving for early retirement: Try 40-30-30.

-

If you have dependents or loans: Adjust savings to 15% temporarily, then increase later.

The goal is not strict compliance — it’s to maintain financial awareness and consistency.

6. Common Mistakes to Avoid

🚫 Counting Wants as Needs:

A Netflix subscription or a new phone isn’t a “need.” Be honest with yourself.

🚫 Not Reviewing Expenses Monthly:

Track your spending regularly to make sure your budget stays balanced.

🚫 Delaying Savings:

Don’t wait for “extra money” to start saving — begin with what you can today.

🚫 Ignoring Inflation:

Revisit your budget every 6–12 months to adjust for rising costs.

7. Tools to Help You Implement the 50-30-20 Rule

Here are some digital tools to automate tracking and budgeting:

-

Walnut / Money Manager: Auto-track income and expenses.

-

ET Money / INDmoney: Manage SIPs, insurance, and investments.

-

Google Sheets: Simple manual budgeting option.

These tools make it easy to stay on top of your financial goals without manual effort.

The 50-30-20 rule is more than just a budgeting formula — it’s a mindset for achieving financial control and freedom.

For salaried professionals, it offers a clear, practical system to manage everyday expenses, enjoy life, and secure the future.

Start today — track your spending, categorize it, and automate your savings. Within a few months, you’ll notice less stress, more savings, and stronger financial confidence.

Remember:

“It’s not about how much you earn, but how wisely you use what you earn.” 💰