How Credit Utilization Impacts Loan Eligibility

When lenders evaluate your loan application, one of the most important factors they check—after your credit score—is your credit utilization ratio. This single number can determine whether you get a loan, how much you qualify for, and the interest rate you receive. Many borrowers unknowingly misuse their credit cards and end up harming their loan eligibility.

Understanding how credit utilization works and managing it smartly can significantly improve your chances of getting approved for loans.

What Is Credit Utilization?

Credit utilization refers to how much of your total credit limit you are using.

Formula:

Credit Utilization Ratio = (Total Credit Used / Total Credit Limit) × 100

Example:

-

Credit Limit: ₹1,00,000

-

Credit Used: ₹60,000

Credit Utilization = 60%

Why Credit Utilization Matters to Lenders

Lenders see credit utilization as a measure of your spending behavior and credit discipline.

A high utilization ratio suggests:

-

You rely heavily on credit

-

You may be facing cash flow issues

-

You could be a high-risk borrower

A low utilization ratio suggests:

-

You are financially stable

-

You use credit responsibly

-

You pose lower risk to lenders

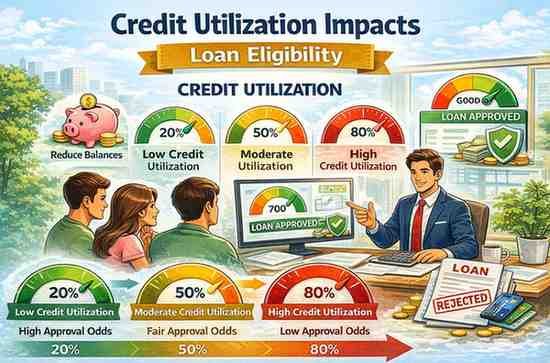

Ideal Credit Utilization Range

Most financial experts—and even lenders—recommend keeping credit utilization:

Below 30% = Excellent

30%–50% = Acceptable

Above 50% = High risk

Above 75% = Very high risk and likely to reduce your credit score

How Credit Utilization Affects Loan Eligibility

1. It Directly Impacts Your Credit Score

Credit utilization contributes 30%–35% of your credit score calculation.

High utilization leads to:

-

Immediate score drop

-

Slow recovery

-

Lower creditworthiness

Even if you pay on time, using 60–90% of your limit regularly can reduce your score and hurt eligibility.

2. High Utilization Signals Potential Financial Stress

Lenders interpret heavy credit usage as a sign that:

-

You may be struggling with expenses

-

You may soon miss payments

-

You depend too much on borrowed money

This reduces your chances of getting:

-

Personal loans

-

Car loans

-

Home loans

-

Business loans

3. Lower Utilization Helps You Qualify for Larger Loan Amounts

When your utilization is low:

-

Your credit score is higher

-

Your financial profile looks stable

-

Lenders trust that you can manage higher EMIs

This improves your loan eligibility significantly, especially for home and car loans where income-to-debt ratio matters.

4. Affects Interest Rates on Loans

Even if your loan is approved, high utilization affects the interest rate offered.

High utilization = High-risk borrower = Higher interest rate

Low utilization = Low-risk borrower = Lower interest rate

Keeping utilization under 30% can help you secure the best interest rates.

5. Influences Pre-Approved Loan Offers

Banks and credit card companies check your credit behavior regularly.

If your utilization is high:

-

Fewer pre-approved offers

-

Lower loan amounts

-

Higher interest rates

If your utilization is low:

-

Higher pre-approved limits

-

Faster approval

-

Attractive rates

How to Manage Credit Utilization Smartly

1. Keep Spending Below 30% of Your Limit

This is the fastest way to improve your credit profile.

Example:

If your card limit is ₹1,00,000 → Try to spend less than ₹30,000.

2. Increase Your Credit Limit (But Don’t Increase Spending)

A higher limit automatically reduces your utilization ratio.

Example:

Limit increased from ₹1,00,000 → ₹2,00,000

Usage ₹40,000 = Only 20% utilization

3. Pay Credit Card Bills Before the Statement Date

Most people pay on the due date — but lenders record utilization on the statement date.

Paying early lowers your reported credit usage.

4. Distribute Expenses Across Multiple Cards

Instead of using one card heavily, divide usage across 2–3 cards to keep each card’s utilization low.

5. Avoid Big Purchases Before Applying for a Loan

Large credit card expenses (even if you plan to repay soon) spike your utilization ratio and lower your score temporarily.

Always keep utilization low 2–3 months before applying for major loans.

6. Convert High Outstanding Amounts Into EMIs

If your card usage is too high, convert it into EMIs to reduce revolving balance and lower utilization.

Credit Utilization and Loan Types

Personal Loans

High utilization is considered risky; lenders may reject applications even with a good salary.

Home Loans

Banks check total utilization while calculating debt-to-income ratio. High usage may reduce eligible loan amount.

Business Loans

Strong credit discipline helps in getting lower interest rates and higher loan limits.

Car Loans

Lower utilization improves chances of getting quick approvals and competitive rates.

Conclusion

Credit utilization is one of the most powerful yet most ignored factors affecting your loan eligibility. By managing it wisely, you can:

-

Improve your credit score quickly

-

Increase your chances of approval

-

Qualify for higher loan amounts

-

Get lower interest rates

-

Build long-term financial stability

The key rule is simple:

Use credit smartly. Keep utilization low. Borrow responsibly.